Hacienda Accepted the Remote Work, Rejected the Tools: The Unanswered Question for Remote Autónomos and Digital Nomads

Most tax discussions start with a simple question: can an autónomo deduct a laptop, a phone, a headset, ChatGPT or other AI tools?

A recent case reviewed by Autonomo.help suggests that these may be the wrong questions entirely.

The more important question may be: how can a remote professional actually prove the business use of the equipment required to perform the work?

After receiving the final decision from Agencia Tributaria, that question remains unanswered.

This article follows our earlier guide on whether autónomos can deduct laptops, phones and AI tools. That first article explained the problem. This one explains what happened after Hacienda issued its final decision.

The Activity Was Real

The taxpayer in this case was a Spanish autónomo providing services remotely to a U.S. company.

This was not a situation involving missing clients, missing invoices or undocumented activity.

The taxpayer provided extensive evidence, including:

- Service agreements with the client

- Confidentiality agreements

- Invoices issued for services

- Documentation explaining the work performed

- Information about remote access to corporate systems

- Descriptions of the software and cloud platforms used during daily work

The taxpayer explained that the work required access to multiple business systems and services, including corporate email, Google Meet, VPN connections, Jira, Confluence, Miro, Slack, Airtable, cloud-based collaboration platforms, professional AI tools and other online services.

The existence of the professional activity was documented in detail.

Most importantly, Agencia Tributaria did not dispute that the work existed.

The taxpayer was genuinely working. The client relationship existed. The invoices existed. The services existed.

This point is critical because it means the dispute was never really about whether the taxpayer was carrying on a business activity.

For more background on invoicing foreign clients, see our guide on how to invoice a client outside Spain as an autónomo.

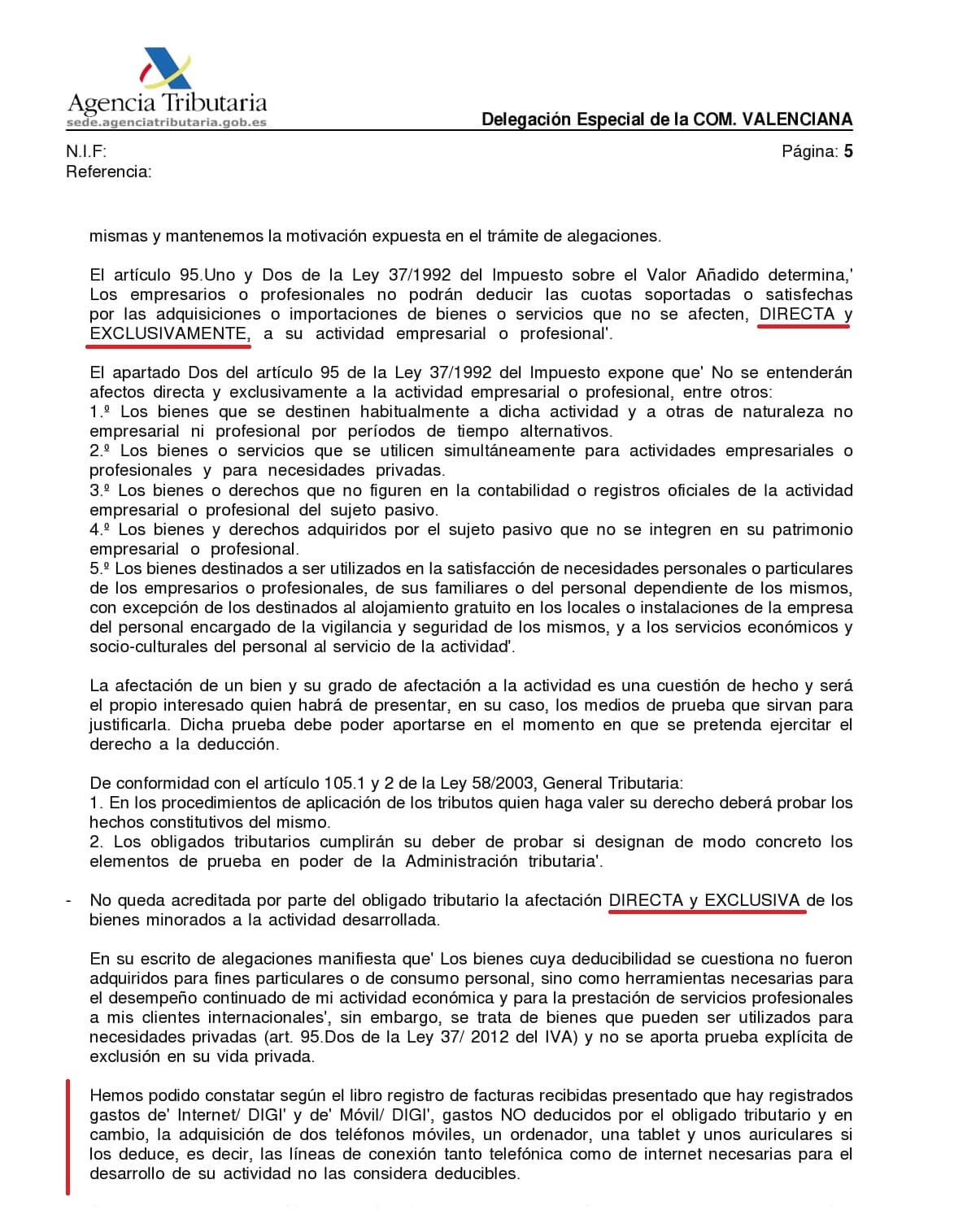

The Equipment Was Rejected

Despite accepting the existence of the professional activity, AEAT rejected VAT deductions relating to:

- A laptop

- Two mobile phones

- A tablet

- A headset with microphone

The reasoning was straightforward.

According to the Tax Agency, these devices are capable of personal use.

As a result, the taxpayer had not sufficiently demonstrated that the equipment was used directly and exclusively for the professional activity.

The adjustment was maintained.

Final decision issued by Agencia Tributaria maintaining the VAT adjustment after reviewing the taxpayer's objections and supporting documentation.

The Damaged Computer

One part of the case makes the rejection especially difficult to understand.

The taxpayer did not simply purchase an additional computer.

Evidence was submitted showing that a previously used computer had been damaged after being delivered to a repair company. Judicial proceedings concerning that damage were already underway, and supporting court documentation was provided to the Tax Agency.

The replacement computer was acquired in order to continue providing services to existing clients.

Nevertheless, the VAT deduction was still rejected.

This is important because the dispute was not only about whether a computer might be useful for remote work. The taxpayer had also explained why a replacement device became necessary.

In other words, the purchase was presented not as an optional upgrade, but as a practical response to the loss of a previously used work device.

The Contract Required a Business Phone

Another important detail concerned the mobile phone.

One of the service agreements explicitly required the contractor to maintain a cellular telephone for business purposes.

The same agreement also contemplated access to company communication systems including Gmail, Calendar and Google Meet.

The agreement further imposed obligations to protect confidential company information from unauthorized access and disclosure.

In other words, the contract itself assumed the existence of communication equipment and remote access tools as part of the work environment.

Yet the VAT deduction for a phone was still rejected.

The Duality at the Center of the Case

This is where the case becomes difficult to reconcile.

On one hand, Hacienda accepted that the taxpayer was performing remote services.

Remote services necessarily involved computers, communication systems, authentication systems, internet access, video conferencing, corporate platforms and cloud-based tools.

On the other hand, Hacienda rejected deductions relating to the equipment used to access those systems.

The practical contradiction

The practical reality of remote work was accepted.

The tools enabling that remote work were not.

The activity existed.

The tools required for the activity were questioned.

The Information Security Problem

The taxpayer also explained that multiple clients, confidentiality obligations and security requirements influenced how equipment was used.

The argument was not that a contract explicitly required two laptops or two phones.

The argument was that separating work environments is a common and reasonable information-security practice.

Modern remote work frequently involves VPN access, multi-factor authentication, corporate credentials, access to confidential business information, segregation of client environments and restricted access systems.

Yet the final decision focused primarily on the absence of proof of exclusive business use.

The broader operational and security context was not considered sufficient.

The Evidence That Was Not Enough

The case is striking because the taxpayer did not rely only on a supplier invoice.

The Tax Agency received explanations and supporting materials relating to the professional activity, client relationships, remote work arrangement, confidentiality duties, digital tools and the damaged computer.

The evidence included contracts, invoices, NDAs, descriptions of VPN access, communication tools, project management systems, cloud platforms and documentation explaining why the replacement computer was needed.

None of this was enough to persuade AEAT that the devices were directly and exclusively connected to the professional activity.

This is why document organization matters. For a broader overview, see our guide on what Hacienda may request after filing Modelo 303.

The Question Hacienda Did Not Answer

The decision explains why the deductions were rejected.

What it does not explain is what evidence would have been enough.

How is an autónomo expected to prove that a particular laptop is used for work?

How is a remote contractor expected to prove that a specific phone is used for authentication, client communications and corporate access?

How does a professional prove that a headset is used for meetings rather than personal entertainment?

Contracts were presented. Invoices were presented. Client relationships were documented. Remote work was documented. Cloud services were documented. Confidentiality obligations were documented. The taxpayer explained how the work was performed.

The decision does not identify what evidence would have changed the outcome.

An Even Bigger Contradiction

Perhaps the most surprising detail is that the Tax Agency specifically noted that internet and telecommunications expenses had not been claimed for VAT deduction.

This observation was used as part of the overall reasoning.

Yet internet access is one of the most obvious prerequisites for remote work.

The decision therefore creates another unresolved question.

If remote work is accepted as genuine, and internet access is required to perform that work, how should an autónomo treat those expenses?

Interestingly, the taxpayer had chosen not to deduct VAT on home internet and telecommunications services, arguably because proving exclusive business use of those services may be even more difficult than proving business use of a laptop or phone.

A home internet connection is typically shared across multiple devices, family members and personal activities. Demonstrating that such a connection is used exclusively for professional purposes may be practically impossible for many remote workers.

This creates a curious contradiction.

The taxpayer did not deduct internet expenses, potentially because they were considered difficult to justify as exclusively business-related.

Yet the decision refers to the absence of those deductions as part of the reasoning supporting the adjustment.

If proving exclusive business use of a laptop is difficult, proving exclusive business use of a home internet connection may be even more challenging.

Again, the decision offers no clear answer regarding what evidence would be sufficient.

Where Should the Line Be Drawn?

The issue also raises a broader practical concern.

Many assets used in professional activities are theoretically capable of personal use.

Computers, telephones, internet connections and communication equipment are obvious examples.

A calculator purchased by an accountant could also be used for personal calculations.

Work clothing purchased by a construction professional could potentially be worn outside a job site.

A mobile phone used for corporate authentication may also be capable of receiving personal calls.

The existence of potential personal use does not automatically answer the more difficult question: whether the asset was acquired and primarily used for the purposes of the economic activity.

If the mere possibility of personal use becomes the dominant factor, taxpayers may reasonably wonder where the line should be drawn.

The final decision does not answer that question.

For more context on quarterly VAT filings, see our guide on how to file Modelo 303 yourself in Spain.

Why This Matters Beyond One Case

This case is not important because a laptop deduction was rejected.

Cases like that happen regularly.

The case is important because it highlights a growing evidentiary problem facing remote professionals.

The modern workplace increasingly consists of computers, phones, cloud platforms, online collaboration tools, AI systems, authentication devices and internet connectivity.

For many professionals, these tools are not merely related to the business.

They are the business.

Yet proving that connection appears to be becoming increasingly difficult.

If you are preparing your quarterly records, our quarterly tax filing checklist for autónomos explains which documents are useful to keep before a review starts.

The Real Lesson

The traditional question is:

Can I deduct a laptop?

The question raised by this case is very different:

If Hacienda accepts that I genuinely work remotely for a foreign client, what evidence must I provide to prove that the computer, phone, headset and internet connection used to perform that work are business assets?

In this case, the taxpayer documented the existence of the professional activity, the client relationship, the invoices, the remote work arrangement and even the need to replace a damaged computer.

Yet the deductions were still rejected.

The final decision does not provide a clear answer.

This uncertainty also explains why some autónomos start looking for shortcuts when buying equipment from other EU countries. For example, they may wonder whether using a Spanish VAT number to buy VAT-free from Germany and then not declaring the purchase would avoid the problem.

We explain why that can create an even bigger VAT issue in our guide on buying VAT-free in Germany using a Spanish VAT number.

And that unanswered question may be the most important lesson for autónomos working in the digital economy.

Related Guides

- Which Business Expenses Are Safest to Deduct as an Autónomo?

- Can Autónomos Deduct Laptops, Phones and AI Tools?

- Hacienda Requested Documents for a VAT Return

- How to Invoice a Client Outside Spain as an Autónomo

- How to File Modelo 303 Yourself in Spain

- Quarterly Tax Filing Checklist for Autónomos in Spain

Preparing Modelo 130 or Modelo 303?

Autonomo.help helps self-employed professionals organize income, expenses, VAT information, and quarterly tax calculations while keeping full control of their documents.

Start Now